Can #Canada and #UnitedStates Mine Enough #RareEarthElements to Meet Future Demand?

As the world accelerates toward electrification and clean energy, rare earth elements (REEs) have become some of the most strategically important minerals on the planet. They are essential components in electric vehicles, wind turbines, smartphones, computers, advanced defense systems, and countless other technologies that power modern life.

A recent study by researchers at the University of Michigan suggests that North America may have the resources needed to build a more self-reliant rare earth supply chain—provided the right economic and policy conditions are in place.

Growing Demand for Critical Minerals

Global demand for rare earth elements is expected to rise significantly over the coming decades. Researchers estimate that worldwide demand will increase from approximately 91 kilotons in 2024 to 123 kilotons by 2030 and 150 kilotons by 2040.

Today, however, the global rare earth industry remains heavily concentrated. China accounts for roughly 70% of global rare earth mining, while the United States contributes only about 11%. This imbalance has raised concerns about supply chain security, economic competitiveness, and national defense readiness.

Assessing North America’s Resource Potential

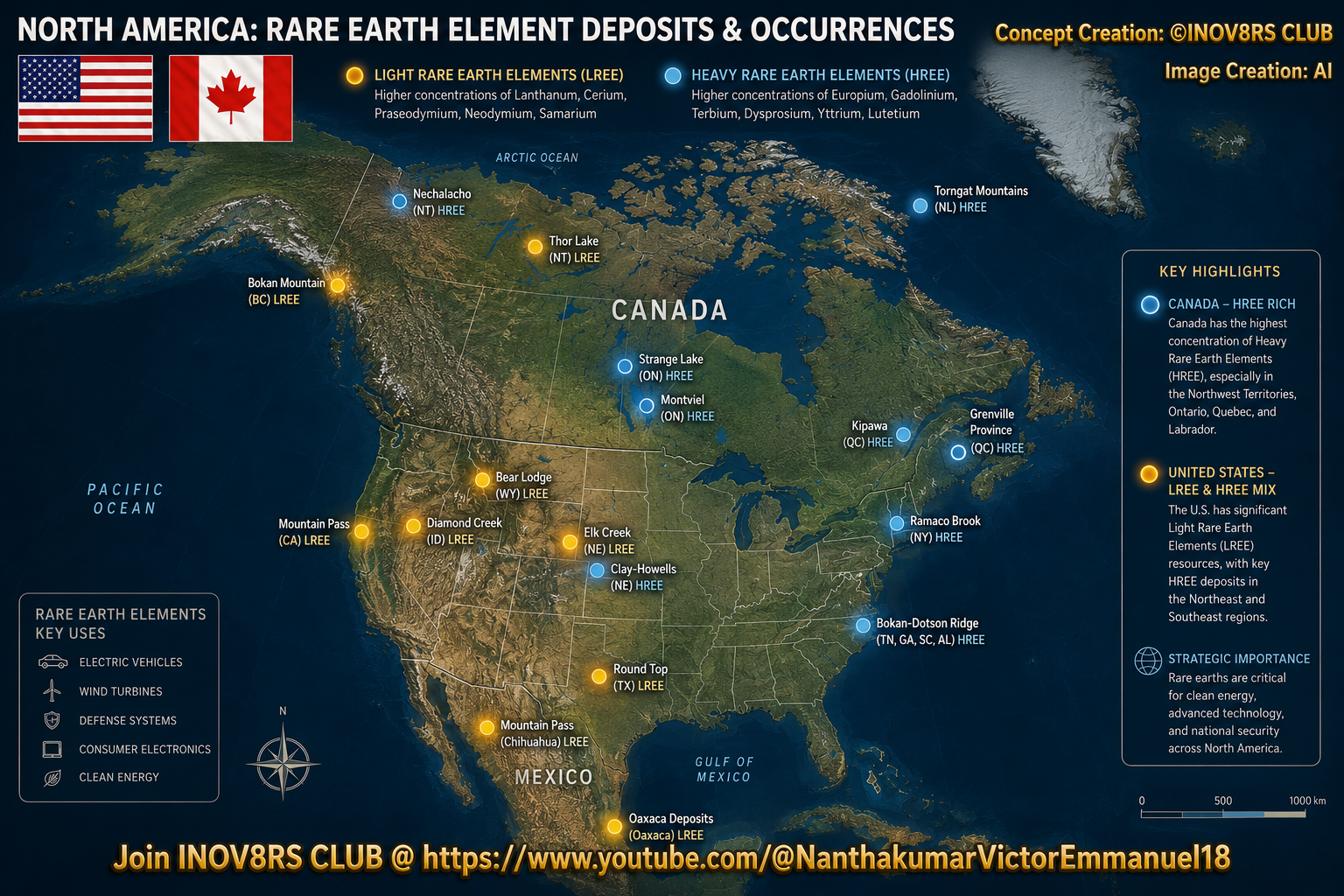

The University of Michigan team evaluated 28 rare earth deposits across North America, analyzing factors such as ore tonnage, mineral grade, and total rare earth oxide content. Their findings indicate that North America possesses enough rare earth resources to satisfy U.S. demand for decades.

The challenge is not the availability of resources, but whether those resources can be extracted economically.

Many North American deposits are lower in quality than leading operations in China and Australia. In addition, some deposits contain elements such as thorium, a naturally occurring radioactive material that can increase mining and disposal costs.

Despite these challenges, researchers believe several deposits could support a competitive domestic supply chain, particularly if governments provide targeted support during the industry’s development phase.

Light vs. Heavy Rare Earth Elements

Rare earth elements are typically divided into two categories: light rare earths and heavy rare earths.

Light rare earth elements are more abundant and are widely used in magnets, batteries, electronics, and renewable energy technologies. Heavy rare earth elements are less common but highly valuable because they improve the performance and heat resistance of high-strength magnets.

The study found a geographic advantage across North America:

- The United States holds substantial deposits of light rare earth elements.

- Canada possesses many of the region’s most significant heavy rare earth deposits.

This distribution suggests that a coordinated North American strategy could strengthen supply security while leveraging the strengths of both countries.

Why Domestic Mining Matters

Rare earth elements are classified as critical minerals because they support industries vital to economic growth, clean energy, and national security. Supply disruptions can have far-reaching consequences, affecting everything from electric vehicle manufacturing to advanced military technologies.

Historically, the United States mined rare earths at California’s Mountain Pass mine, but much of the industry’s processing capacity eventually shifted overseas. Today, experts argue that rebuilding domestic mining alone is not enough. North America must also develop processing, refining, and manufacturing capabilities to create a fully integrated supply chain.

The Path Forward

The study concludes that North America has the geological resources needed to establish a more resilient rare earth industry. However, success will depend on balancing economic viability, environmental responsibility, and strategic investment.

As demand for electric vehicles, renewable energy systems, and advanced technologies continues to grow, developing a secure domestic supply of rare earth elements could become one of the most important industrial challenges—and opportunities—of the coming decades.