#Trump Executive Order Strengthens the #US #Defense Supply Chain

The U.S. defense supply chain has become one of the country’s most important national security priorities. From fighter jets and missile systems to military communications and cybersecurity infrastructure, every defense program relies on a complex network of suppliers around the world.

A new executive order issued by the Trump administration seeks to strengthen the U.S. defense supply chain by identifying vulnerabilities, reducing dependence on foreign suppliers, and improving the resilience of America’s defense industrial base.

As geopolitical tensions continue to reshape global manufacturing, securing the defense supply chain has become a strategic objective for both policymakers and defense contractors.

Why the Defense Supply Chain Matters

Modern military equipment depends on thousands of specialized components sourced from multiple countries. These include:

- Advanced semiconductors

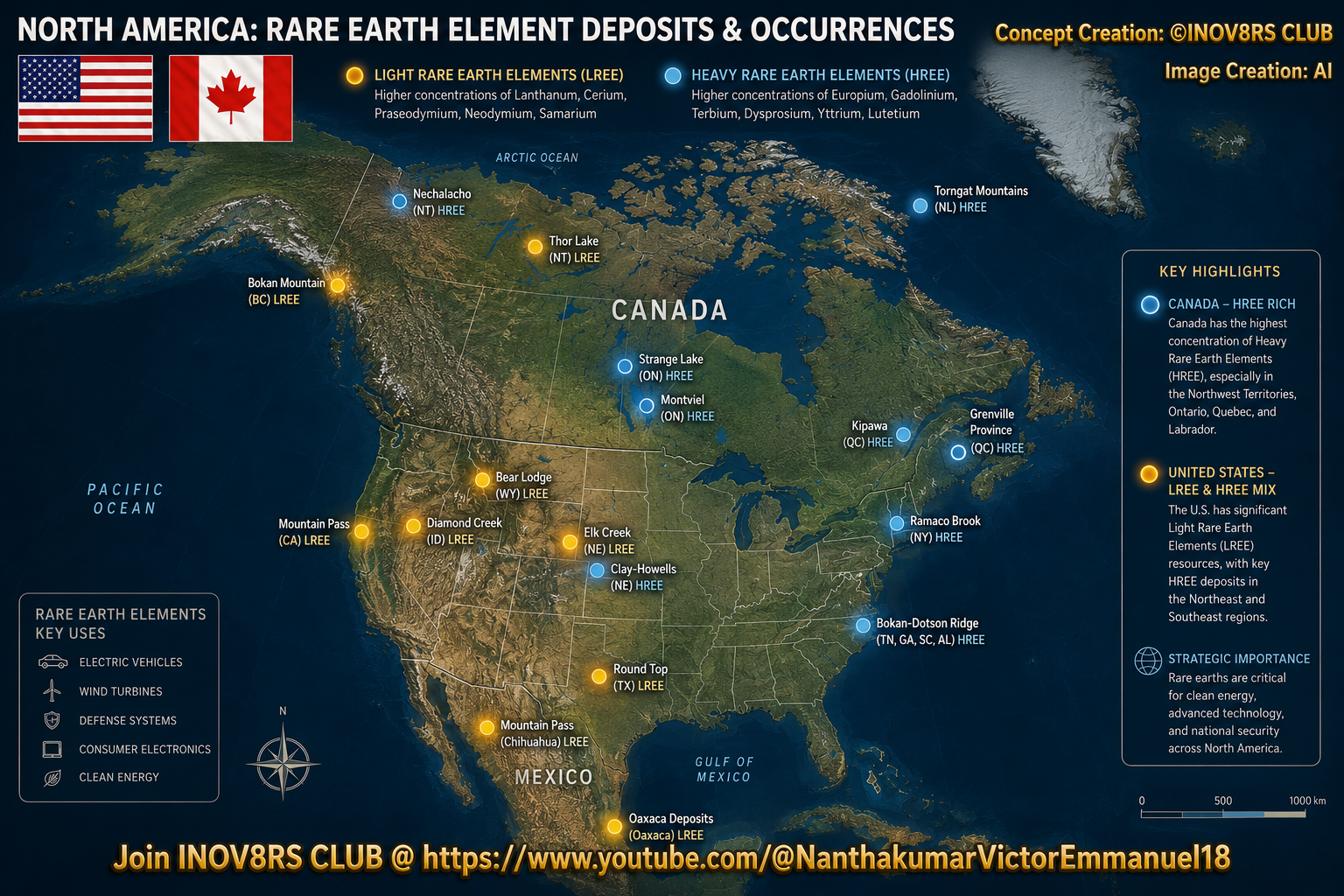

- Rare earth elements

- Critical minerals

- Precision electronic components

- Aerospace materials

A disruption affecting even one supplier can delay production of essential defense systems. Whether caused by geopolitical conflict, trade restrictions, cyberattacks, or natural disasters, supply chain interruptions can directly impact military readiness.

This is why governments around the world are investing heavily in supply chain resilience.

What the Executive Order Does

The executive order directs federal agencies and defense contractors to improve visibility across their supplier networks and identify potential vulnerabilities.

Key objectives include:

- Mapping defense supply chains from raw materials to finished products

- Reducing reliance on suppliers located in strategic competitor nations

- Strengthening domestic manufacturing capabilities

- Improving risk assessments for critical defense materials

- Enhancing long-term resilience across the defense industrial base

The overall goal is to ensure that military production can continue even during periods of international instability.

Reducing Dependence on Foreign Suppliers

One of the primary concerns addressed by the policy is America’s dependence on overseas sources for materials essential to defense manufacturing.

These include:

- Rare earth elements

- Lithium

- Graphite

- Titanium

- Nickel

- Cobalt

- Specialized electronic components

Many of these resources are concentrated in a limited number of countries, creating potential supply chain bottlenecks.

Diversifying suppliers and expanding domestic production could reduce these risks while supporting long-term national security objectives.

Why Critical Minerals Are Strategically Important

Critical minerals are essential for manufacturing modern defense technologies, including:

- Radar systems

- Missile guidance systems

- Aircraft electronics

- Naval equipment

- Satellite communications

- Advanced batteries

Without reliable access to these materials, production delays could affect military procurement programs.

For this reason, governments increasingly view critical minerals as strategic assets rather than ordinary commodities.

Potential Benefits of a Stronger Defense Supply Chain

If successfully implemented, the executive order could deliver several long-term advantages.

Improved National Security

A more resilient supply chain reduces the risk that international events will interrupt military production.

Faster Defense Manufacturing

Greater supply chain visibility helps manufacturers identify bottlenecks before they become production delays.

Increased Domestic Investment

Policies encouraging domestic sourcing may stimulate investment in U.S. mining, manufacturing, semiconductor production, and advanced materials.

Better Risk Management

Defense contractors can make more informed procurement decisions by understanding supplier dependencies throughout their production networks.

Challenges Facing Implementation

Strengthening the defense supply chain is not a short-term effort.

Many defense systems rely on highly specialized suppliers that have developed expertise over decades. Replacing those suppliers or relocating production requires significant investment, workforce development, regulatory approvals, and years of planning.

Organizations must also balance resilience with affordability, ensuring that increased security does not lead to excessive procurement costs.

The Future of U.S. Defense Manufacturing

Global supply chains are becoming increasingly intertwined with national security policy.

Governments are placing greater emphasis on domestic manufacturing, trusted international partnerships, and transparent supplier networks to reduce strategic risk.

For defense contractors, this means supply chain management is evolving from an operational concern into a core element of long-term business strategy.

Conclusion

The Trump administration’s executive order reflects a broader shift toward strengthening the U.S. defense supply chain and reducing vulnerabilities in critical defense manufacturing.

While implementation will take time, the initiative highlights a growing consensus that supply chain resilience is essential for military readiness, technological leadership, and national security in an increasingly uncertain global environment.

Source: The Washington Post