Fears of China choking off exports of critical minerals to Japan amid a deepening political dispute have set off industry alarms and prompted Tokyo to elevate the issue at a G7 gathering of finance ministers this week, despite Beijing’s assurances that civilian trade would be spared.

Japanese Finance Minister Satsuki Katayama said last week that she would attend the Group of Seven event in Washington on Monday with the “risk of a rare-earth-supply interruption from China in mind”, the Tokyo-based Jiji Press reported. Officials from Canada, the United States and Australia were also expected to participate.

The inclusion of rare earths on the G7 agenda reflects heightened concern in Japan over China controlling exports of 17 rare earth elements that are crucial for Japan’s massive manufacturing sector, from consumer electronics to vehicles, according to analysts.

Although Japan has reduced its reliance on Chinese rare earths since 2010, when China stopped rare earth exports for two months following a vessel collision near disputed islets, it still depends heavily on Chinese supplies, as replacements take time, the experts said.

The Chinese State Council’s “Rare Earth Industry Development Plan (2021-2025)” establishes coordinated targets that explicitly connect mining output with downstream technology milestones. This policy framework differs from market-driven approaches where private investment decisions occur independently of government industrial planning.

Key coordination mechanisms include:

Research funding allocation aligned with five-year industrial development priorities

State-owned enterprise operations integrated with private sector innovation incentives

Regulatory environments designed to support domestic technology development clusters

University-industry partnerships with explicit commercialization mandates

Government research institutes, including Chinese Academy of Sciences divisions focused on materials science, receive dedicated funding for rare earth materials research aligned with broader industrial objectives. This creates predictable resource flows for long-term research projects while ensuring alignment between fundamental research and commercial applications.

The integration extends to environmental and regulatory considerations. Chinese facilities operate under different environmental compliance requirements compared to Western competitors, enabling cost structures that support both current operations and reinvestment in technology development. Additionally, these operations increasingly benefit from decarbonization benefits that enhance long-term competitiveness. This regulatory environment, combined with established supply chains and vertical integration advantages, creates compound benefits for innovation funding.

How Does China’s Patent Strategy Create Competitive Moats in Critical Technologies?

Intellectual Property Accumulation in Emerging Materials

China’s patent filing activity in rare earth materials significantly exceeds Western competitors, with China accounting for approximately 40-50% of global rare earth materials patents and higher percentages in emerging technology areas including nanomaterials and energy storage applications, according to World Intellectual Property Organization data from 2023.

Patent applications in rare earth nanomaterials and energy storage categories have grown at approximately 15-20% year-over-year in China between 2018-2023, while Western filing rates in equivalent categories have remained relatively flat or declined. This divergence reflects different strategic approaches to materials innovation and intellectual property development.

Focus areas for Chinese patent activity include:

Energy storage nanomaterials with enhanced conductivity and thermal stability

Magnetic separation processes optimizing cost structures and efficiency

Luminescent compounds for specialized optical and sensor applications

Advanced alloy compositions targeting aerospace and electronics sectors

Consequently, organizations must develop comprehensive IP protection strategies to safeguard their technological advantages in this competitive landscape.

Research Institution Networks and Knowledge Transfer

Chinese university-industry collaboration operates under different structural incentives compared to Western academic systems. Chinese institutions receive explicit mandates to commercialize research findings, supported by government incentive structures that reward technology transfer activities. This contrasts with Western university systems where commercialization typically occurs post-publication through licensing offices, creating longer development timelines.

WASHINGTON, Jan 11 (Reuters) – U.S. Treasury Secretary Scott Bessent will urge Group of Seven nations and others to step up their efforts to reduce reliance on critical minerals from China when he hosts a dozen top finance officials on Monday, a senior U.S. official said.

The meeting, which kicks off with a dinner on Sunday evening, will include finance ministers or cabinet ministers from the G7 advanced economies, the European Union, Australia, India, South Korea and Mexico, said the official who was not authorized to speak publicly.

Together, the grouping accounts for 60% of global demand for critical minerals.

“Urgency is the theme of the day. It’s a very big undertaking. There’s a lot of different angles, a lot of different countries involved and we really just need to move faster,” the official said.

Oklahoma’s emergence as a critical minerals hub represents a strategic convergence of geographic advantages, established infrastructure, and national security imperatives. The state’s positioning within North American transportation networks, combined with abundant energy resources and experienced industrial workforce, creates unique opportunities for domestic processing operations that reduce import dependencies while supporting defense manufacturing requirements.

Oklahoma’s emergence as a strategic processing hub demonstrates how transportation networks and energy infrastructure create multiplicative advantages for critical minerals operations. The state’s positioning at the intersection of continental transportation corridors provides unprecedented access to both raw material sources and end-user markets across North America.

Chemical processing expertise from Oklahoma’s refining and petrochemical operations transfers directly to mineral separation and purification systems. Workers experienced in hydrocarbon separation, distillation, and reduction chemistry possess foundational knowledge for solvent extraction, precipitation, and crystallization processes essential to lithium, nickel, and rare earth processing.

Environmental compliance experience accumulated through decades of Clean Air Act and Clean Water Act requirements in energy operations reduces training requirements for mineral processing facilities. The regulatory framework familiarity and OSHA certification systems provide established pathways for workforce transition rather than development from baseline.

Canada Nickel has amassed almost four billion tonnes in nickel resources in the ground around Timmins.

Just before Christmas, the Toronto multi-mine developer published mineral resources for more two deposits, Midlothian and Bannockburn, both situated south of the city.

Like Canada Nickel’s other properties in the area, including its flagship Crawford project, the Midlothian and Bannockburn projects are shaping up to be low-grade, big-tonnage type of nickel deposits.

To date, Canada Nickel has posted resource estimates on eight of its nine properties in the region.

That amounts to 3.98 billion tonnes of 0.24 per cent nickel in the measured and Indicated resources, for a total of 9.4 million tonnes of nickel metal. There’s an inferred resource of 4.95 billion tonnes of 0.23 per cent nickel, for a total of 11.5 million tonnes of contained nickel metal.

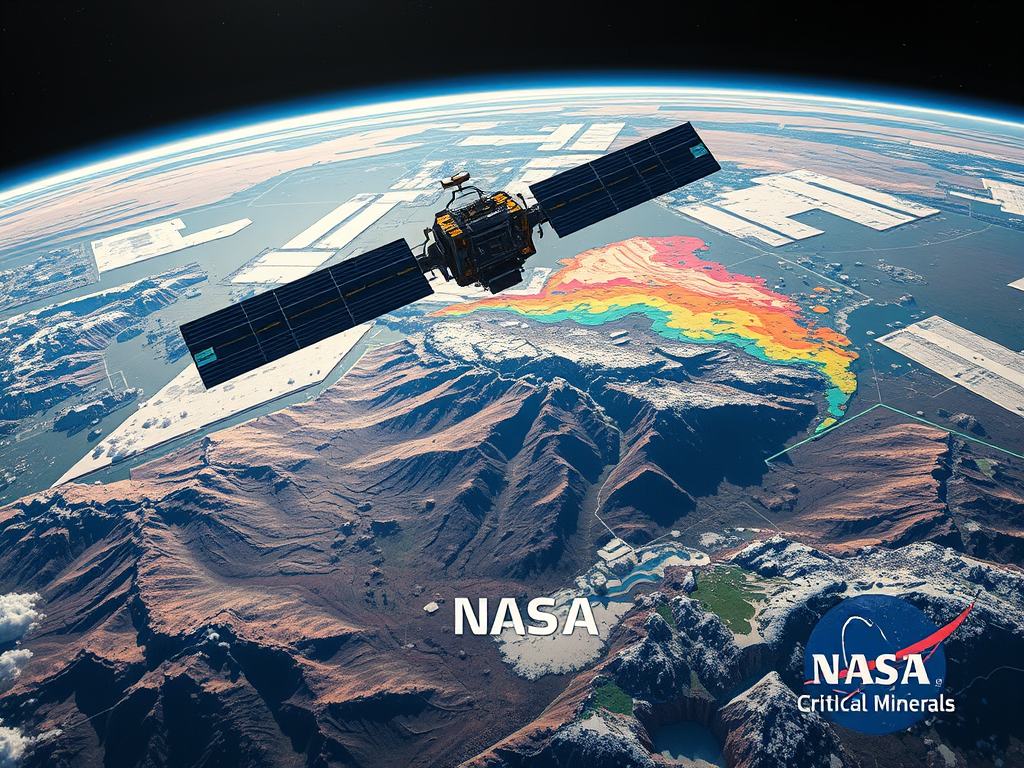

NASA mineral mapping technology represents a groundbreaking advancement in mineral exploration, utilising hyperspectral imaging to identify critical battery materials from stratospheric altitudes. This technology captures electromagnetic radiation across 224 contiguous spectral bands, enabling detection of lithium, cobalt, and titanium compounds across vast geographic regions whilst accelerating discovery timelines that traditionally required decades of ground-based exploration.

NASA mineral mapping technology operates fundamentally differently from conventional satellite imaging through its ability to capture electromagnetic radiation across 224 contiguous spectral bands spanning 400-2,500 nanometres. Traditional satellite systems like Landsat utilise only 11 spectral bands, while Sentinel-2 operates with 13 bands, creating significant limitations in mineral identification capabilities.

Presently, there are a few small Indian companies engaged in manufacturing rare earth magnets. The industry needs a big push to feed the new generation of industries – from electric vehicles to fighter aircraft engines, wind turbines, and laptops to mention a few. Lately, it has come into a big focus as the world is moving towards electric vehicles. Rare earth magnet is a crucial component of electric vehicles (EVs). Fortunately, India has large rare earth deposits. Globally, it ranks third after China and Brazil.

The demand for rare earth magnets in India is expected to increase sharply in the coming years, driven by the expansion of EV manufacturing, increasing electronics output, defence production, industrial automation and renewable energy generation. For the present, the country uses rare earth magnets to the extent of 4,000 tonnes per year, mostly through imports. Among the companies currently manufacturing rare earth magnets in India are: IREL (India) Limited, Permanent Magnets Limited, Ashvini Magnets Private Limited, Star Trace, Eriez Magnets, Kumar Magnet, Sonal Magnetics, A to Z Magnet Mfg. Co. and Pragati Enterprises. The demand for rare earth magnets is projected to double by 2030. Lately, China has imposed restrictions on exports. Earlier this year, China slapped export licenses for seven types of rare earth elements and derivative products.

A group of battery metal exploration companies and startups says it has a plan to turbocharge Canada’s critical minerals sector by building out “midstream” mineral processing facilities in Western Canada.

Two reports published by the Battery Metals Association of Canada, which hired analysts at the Transition Accelerator to consult with their members, identified nine critical minerals — copper, graphite, iron, nickel, lithium, phosphate, rare earths and vanadium — and five regions where they see big opportunities for major projects.

For example, British Columbia has at least four producing copper mines, which all ship their copper concentrate overseas, primarily to China, because there are no smelters in Western Canada. Building a copper smelter could encourage copper production and exploration while also creating higher-value products to sell, the reports said.

“If you wanted to put together a critical minerals processing behemoth anywhere in the world, the assets that we have in Alberta to do that are just phenomenal,” Bentley Allan, a professor of political economy at Johns Hopkins University and a principal at Transition Accelerator, said. “It has the chemical processing expertise, the clean power resources, other kinds of machining and precision instruments, which make Alberta a really incredible place to do this.”

The Canadian province of Saskatchewan has vowed to compete with China in processing and production of rare earths and become the first North American commercial alternative source for the metals, used to make magnets for electric vehicles and wind turbines.

The Saskatchewan Research Council Rare Earth Processing facility is betting on demand for these magnets to jump in the next couple of years, driven by demand from original equipment manufacturers such as automakers.

The SRC Rare Earth processing facility has begun production on a commercial scale and expects to hit a production target of 40 tonnes of rare earth metals per month by the end of this year. And it will produce 400 tonnes of the NdPr metals per year, which is enough to produce 500,000 EVs, according to SRC. The facility has already tied up with potential clients in South Korea, Japan and the United States.

BHP Billiton is understood to have made a substantial copper discovery in the remote West Australian outback, in a move that could finally help open up the potential of the West Musgrave region.

Industry sources told The Australian that recent drilling by BHP at the Succoth prospect had returned broad intersections of copper mineralisation at relatively high grades.