Is #America’s Defense Industrial Base Ready for War? The Critical Role of #RareEarthElements and #Innovation

Lessons from the 2026 CSIS Progress Report

The phrase “wartime footing” has become increasingly common in U.S. national security discussions. But what does it actually mean? More importantly, is the United States making meaningful progress toward building an industrial base capable of supporting prolonged, high-intensity conflict?

A recent report by the Center for Strategic and International Studies (CSIS), Is the Industrial Base on a Wartime Footing? A Progress Report, offers a detailed assessment of how the U.S. defense industrial base has evolved since the Department of Defense announced this objective in late 2025.

What Does “Wartime Footing” Mean?

A wartime industrial base is one that can rapidly produce, replenish, and sustain military capabilities during extended conflict. This requires more than simply increasing defense spending—it demands resilient supply chains, modern manufacturing, strong public-private partnerships, and a steady pipeline of innovation.

According to the report, the Pentagon has made significant progress through industrial policy reforms, acquisition modernization, and increased investment in both traditional and nontraditional defense companies.

Signs of Real Progress

Several developments suggest that the U.S. defense industrial base is becoming more dynamic:

- Approximately 10,000 new firms have entered the defense market over the past two years.

- Nontraditional defense companies received more than $120 billion in contract obligations during FY2025.

- Munitions contract obligations have increased by 330% since FY2010.

- The Department of Defense is increasingly using multiyear procurement agreements to encourage manufacturers to expand production capacity.

These initiatives signal a shift toward creating predictable demand that encourages industry to invest in long-term manufacturing capacity.

Defense Spending Is Growing—but Is It Enough?

While defense spending has increased substantially in absolute dollars, it has remained relatively stable as a percentage of GDP. The report argues that true wartime footing would require spending levels closer to 4.6% of GDP, as proposed in the FY2027 budget request, compared with approximately 3.1% in 2025.

International comparisons illustrate the gap:

- Ukraine, Israel, and Russia currently devote much larger shares of their economies to defense.

- The United States remains above most allies but below countries actively engaged in sustained conflict.

Munitions: The Critical Bottleneck

One of the report’s strongest messages concerns munitions production.

Although funding has increased dramatically, manufacturing timelines remain lengthy. Many advanced missiles still require 25 to 51 months from production start to delivery. Meanwhile, recent conflicts have exposed the vulnerability of existing stockpiles, particularly for missile defense interceptors like Patriot and THAAD.

To address these challenges, the Pentagon is:

- Expanding missile production capacity.

- Investing in new manufacturing facilities.

- Supporting affordable, high-volume weapon systems.

- Accelerating domestic drone production.

The strategic emphasis is shifting from simply producing highly sophisticated weapons to balancing quality with affordability and scale.

Strengthening the Supply Chain

A resilient defense industry depends on more than final assembly lines.

The report highlights growing investment in the solid rocket motor sector, where new entrants such as emerging manufacturers are helping diversify production and reduce bottlenecks. Government investment, multiyear procurement agreements, and direct capital support are being used to encourage competition and increase capacity.

This represents a broader shift from relying on a small number of legacy suppliers toward developing a more competitive industrial ecosystem.

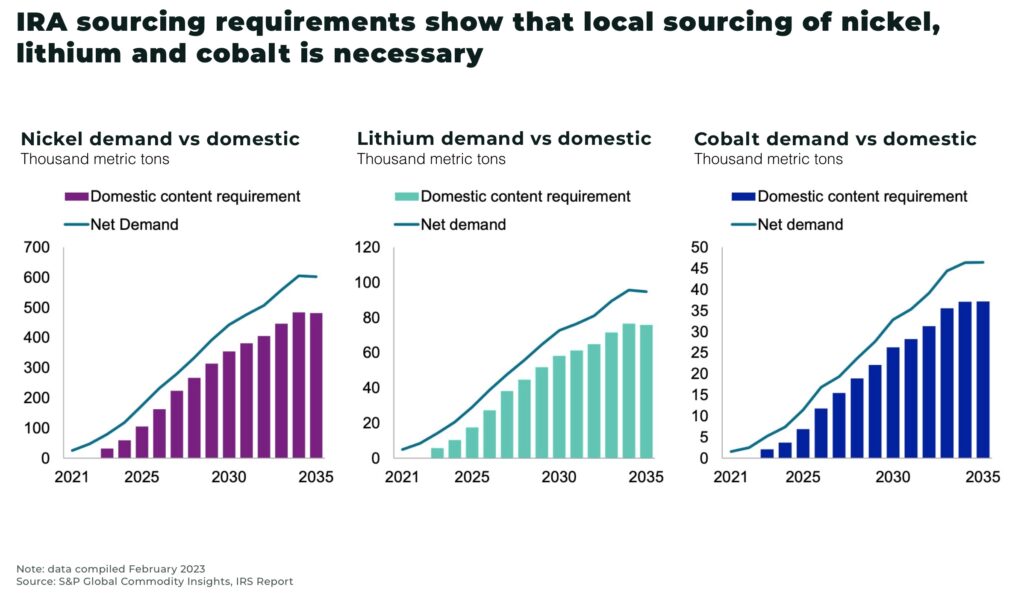

The Rare Earth Challenge

Perhaps the most strategic vulnerability identified is America’s dependence on China for rare earth materials.

Rare earth elements are essential for advanced military technologies, including guided missiles, radar systems, electric motors, and numerous defense electronics.

To reduce this dependence, the U.S. government has significantly expanded investment in domestic production and processing:

- Announced government commitments reached approximately $7.6 billion during 2025–2026.

- This represents a 321% increase compared with the previous four years.

- New initiatives aim to build a complete domestic “mine-to-magnet” supply chain.

While encouraging, the report emphasizes that rebuilding an industry lost over several decades will require sustained effort over many years.

Allies Matter

The report also stresses that industrial resilience cannot be achieved alone.

Foreign military sales have increased by 347% since FY2015, reflecting stronger defense cooperation with allies and partners. Beyond exports, the United States is expanding joint production, co-development, and shared industrial initiatives with countries including Canada, Finland, and South Korea.

International collaboration is increasingly viewed as an essential component of industrial resilience rather than simply a diplomatic tool.

The Bottom Line

The CSIS report concludes that the United States has made genuine progress toward building a wartime-ready industrial base. Defense investment is increasing, acquisition reforms are accelerating, manufacturing capacity is expanding, and critical supply chains are receiving renewed attention.

However, important challenges remain:

- Production lead times are still measured in years.

- Critical munitions inventories remain insufficient.

- Rare earth supply chains are only beginning to diversify.

- Industrial reforms must consistently translate investment into sustained production capacity.

Ultimately, wartime readiness is not a milestone that can simply be declared—it is an ongoing process requiring long-term commitment from government, industry, and allied partners. The strength of America’s future deterrence will depend not only on technological superiority but also on its ability to manufacture, replenish, and sustain military capability faster than potential adversaries.

Source: CSIS