A small Northern Ontario community is set to play a major role in North America’s clean energy future.

Electra Battery Materials is moving forward with plans to build North America’s first battery-grade cobalt refinery in Cobalt, Ont., with commercial operations expected to begin by the end of 2027. Once operational, the facility will produce up to 6,500 tonnes of cobalt sulfate annually—enough to supply approximately one million electric vehicle batteries each year.

A milestone for North America’s battery industry

The refinery will be the first of its kind in North America and only the second battery-grade cobalt refinery outside China. The project marks a significant step toward strengthening the continent’s critical mineral supply chain as demand for electric vehicles, energy storage systems and advanced technologies continues to grow.

Electra says the refinery will process cobalt hydroxide sourced from the Democratic Republic of the Congo (DRC), with the material shipped through South Africa and Montreal before being refined in Canada.

Reducing reliance on China

China currently dominates global cobalt refining, processing more than 75 per cent of the world’s supply. By establishing refining capacity in Canada, the project aims to diversify supply chains and improve North America’s access to a mineral considered essential for electric vehicles, consumer electronics and defence technologies.

Electra CEO Trent Mell says critical minerals have become increasingly important not only for transportation and renewable energy, but also for national security.

The refinery has received financial support from both the Canadian and U.S. governments, reflecting growing efforts to build more resilient domestic supply chains for critical minerals.

Industry sees both opportunity and challenges

While demand for cobalt is expected to increase, some industry experts note that evolving battery technologies could reduce future dependence on the metal. Others point to ongoing concerns surrounding cobalt mined in the DRC, particularly related to human rights and responsible sourcing.

Electra says it is committed to responsible procurement practices and believes cobalt will remain a critical material, particularly as demand grows in defence applications alongside the electric vehicle market.

A new chapter for the town of Cobalt

The refinery also represents an economic transformation for the historic mining community of Cobalt. Once one of the world’s leading silver-producing regions following the area’s famous 1903 discovery, the town is now positioning itself as a key hub in North America’s battery materials industry.

Although commercially viable local cobalt reserves have yet to be developed, the new refinery could help establish Cobalt as an important processing centre, supporting Canada’s broader strategy to strengthen its critical minerals sector and secure the supply chain for next-generation technologies.

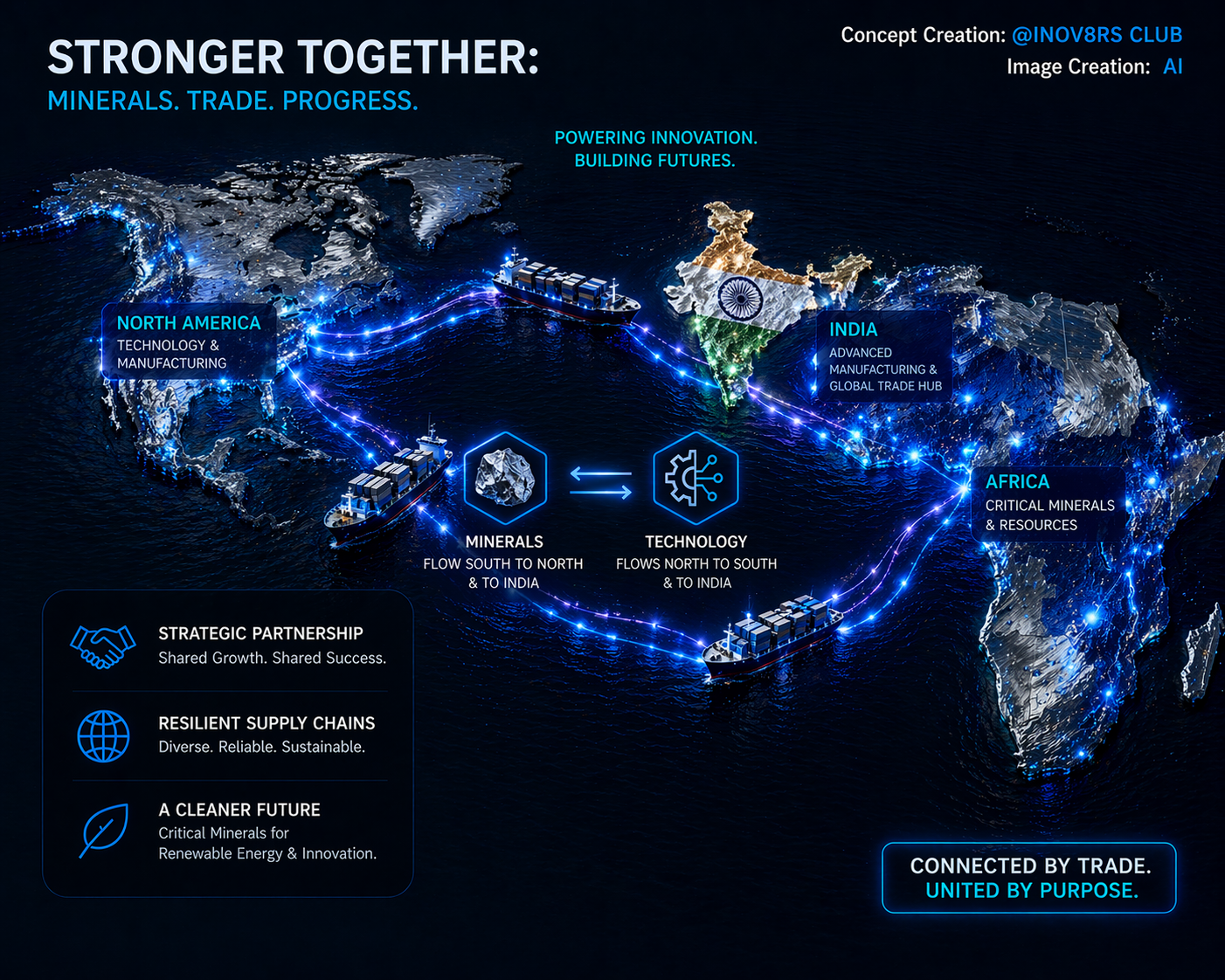

The Democratic Republic of Congo (DRC) is no longer content with being merely the world’s largest cobalt supplier. Through a combination of export controls, strategic partnerships, and geopolitical repositioning, Kinshasa is transforming its role from resource provider to market maker.

The implications extend far beyond commodity markets. Congo’s evolving cobalt strategy is influencing global supply chains, altering China’s dominance in critical minerals, and creating new opportunities for Western investors seeking secure access to strategic resources.

From Price Taker to Price Setter

For years, Congo’s vast cobalt reserves fueled global battery production while the country remained vulnerable to commodity price cycles and foreign influence. That dynamic is changing.

Since imposing cobalt export restrictions in early 2025, Congo has steadily tightened control over the flow of the metal. A complete export ban eventually gave way to a quota system, but the impact on global supply has been profound.

China, historically the dominant buyer of Congolese cobalt, has seen imports collapse. Customs data show that Chinese imports of Congolese cobalt intermediates during the first four months of 2026 were only a fraction of the volumes recorded during the same period a year earlier.

The result has been a dramatic tightening of supply. Cobalt prices have more than doubled from pre-restriction levels, while unusual pricing patterns have emerged throughout the supply chain. Cobalt hydroxide—the primary form exported from Congo—has at times traded at prices equal to or even above refined cobalt metal, highlighting growing concerns about access to raw material.

What initially appeared to be a temporary supply disruption increasingly looks like a structural shift. Market participants are beginning to attach a premium to cobalt sourced from Congo, reflecting both scarcity and strategic importance.

Reducing Dependence on China

Perhaps the most significant aspect of Congo’s strategy is its attempt to diversify away from overwhelming dependence on Chinese operators.

China has spent decades building a dominant position in Congolese mining and refining. Chinese companies control many of the country’s largest cobalt and copper assets, while Chinese refiners process much of the world’s cobalt supply.

Now, however, Kinshasa appears determined to rebalance those relationships.

Recent developments suggest growing momentum behind Western investment initiatives. U.S.-based critical minerals platform Virtus Minerals recently acquired the copper and cobalt assets of Chemaf, positioning itself to revive operations that have faced years of uncertainty.

At the same time, Congo’s state-backed Entreprise Générale du Cobalt (EGC) has entered into agreements with commodity trader Trafigura and U.S. startup EVelution to support a proposed cobalt refinery in Arizona. Such projects could create direct links between Congolese mines and American manufacturing, reducing reliance on Chinese processing capacity.

These developments align closely with broader U.S. efforts to secure critical mineral supply chains amid intensifying competition with China.

Infrastructure Creates New Options

Infrastructure is playing a crucial role in Congo’s westward pivot.

The Lobito Atlantic Railway, backed by Western governments and investors, is emerging as a strategic alternative export route. Connecting the Congolese copper belt to Angola’s Atlantic port of Lobito, the corridor provides access to global markets without relying exclusively on transport networks historically aligned with Chinese interests.

The railway has become a symbol of a larger geopolitical contest over critical minerals. Control over extraction matters, but so does control over logistics, processing, and market access.

For Western investors, the corridor offers a practical pathway for moving minerals to Europe and North America. For Congo, it provides leverage and flexibility.

Solving the Artisanal Mining Challenge

Despite these opportunities, one major obstacle remains: artisanal and small-scale mining (ASM).

Artisanal miners produce a significant share of Congo’s cobalt, but the sector has long been associated with unsafe working conditions, child labor concerns, and informal trading networks. These issues have discouraged many Western buyers from sourcing Congolese cobalt directly.

The government understands that expanding access to Western markets requires stronger assurances around responsible sourcing.

To address this challenge, EGC has partnered with commodity trader Mercuria to establish what is being described as a “gold standard” framework for ethical artisanal cobalt production at the Kasulo mining site.

Success is far from guaranteed. Previous efforts to formalize the artisanal mining sector have delivered mixed results. However, creating a transparent and verifiable supply chain is essential if Congo hopes to attract Western customers seeking ethically sourced critical minerals.

The stakes are high. Without credible solutions, concerns over “blood cobalt” could continue limiting market access regardless of supply shortages.

Growing Leverage in a Tightening Market

Congo’s position is being strengthened by supply disruptions elsewhere.

Several competing sources of cobalt face challenges. Canadian producer Sherritt International’s refining operations have come under pressure from U.S. sanctions affecting its Cuban partnerships. Madagascar’s Ambatovy nickel-cobalt project suffered cyclone-related disruptions and is undergoing ownership changes. Meanwhile, Indonesian producers are grappling with tighter mining quotas and processing constraints.

These developments further increase Congo’s influence over a market where it already accounts for more than 70% of global mine production.

In other words, there are few realistic alternatives.

A New Strategic Role

The broader story is not simply about higher cobalt prices. It is about a country leveraging its resource dominance to reshape its geopolitical position.

By restricting exports, encouraging Western investment, developing alternative infrastructure, and attempting to formalize artisanal production, Congo is seeking greater control over both its resources and its future.

Whether the strategy succeeds remains uncertain. Balancing relationships with China while attracting Western capital will require careful diplomacy. Reforming the artisanal mining sector will be difficult. And sustaining investor confidence will depend on political stability and regulatory consistency.

Yet one thing is increasingly clear: Congo is no longer just supplying the global cobalt market. It is actively redefining it.

As demand for batteries, electric vehicles, defense technologies, and advanced electronics continues to grow, Congo’s decisions will have an outsized influence on the future of critical minerals. The country is emerging not merely as a producer of cobalt, but as one of the most important strategic players in the global race for resources.

This version is designed for a business, commodities, mining, or geopolitical affairs audience and is fully original rather than a rewrite of the Reuters text.

The DRC, one of Africa’s most resource-rich jurisdictions, has positioned AI at the centre of its exploration strategy. Speaking at last year’s AMW the country’s Minister of Mines said AI-enabled exploration has the potential to reduce resource-discovery timelines to under three years, and that the government is working to unlock 90 per cent of DRC’s geology and more than US$24 trillion in untapped mineral value.

Recent deployments back the rhetoric. In February 2026, the DRC partnered with Xcalibur Smart Mapping to use advanced geospatial solutions for mapping critical minerals and lowering exploration risk. The country is also working with US-based startup KoBold Metals to apply AI-driven techniques at the Mingomba Lithium Mine.

Zambia, Ghana, Botswana, and Burundi

The trend extends beyond DRC. KoBold Metals is also applying AI at Zambia’s Mingomba Copper Project to identify high-grade deposits, backing the government’s push to lift annual copper output to three million tonnes by 2031. Burundi has partnered with KoBold and Lifezone Metals to digitise its geological database and assess the 140-million-tonne Musongati Nickel Project.

In Ghana, the Ghana Gold Board and the Ghana Geological Survey Authority are using AI-assisted mineral prospectivity modelling across the Funsi, Atuna, and Bensere East concessions, aligning with a national drive to expand gold reserves and production.

Botswana is using the same tool-set to diversify away from diamonds. Botswana Minerals has identified eight new copper deposits through AI-powered exploration, accelerating the country’s move into critical minerals.

The capital pitch

The underlying economic pitch is large. Organisers estimate Africa sits on $8.5 trillion in untapped mineral resources, and point to the continent’s 30 per cent share of global critical minerals at a moment when demand is projected to triple by 2030. AI’s role, AMW’s 2026 programming suggests, is to compress exploration cycles, reduce the cost of de-risking ground, and tighten operational efficiency once mines are producing.

The Democratic Republic of Congo will create a paramilitary unit to police its mines with funding from the US and United Arab Emirates, the country’s General Inspectorate of Mines said.

The agency will invest $100 million and deploy as many of 3,000 armed recruits by December, with a goal of 20,000 “mining guards” around the country by 2028, it said in an emailed statement on Monday.

The force will secure production, ensure traceable transport of minerals, and replace “defense forces currently deployed in mining zones,” according to the statement.

Police currently patrol most operations, but military and presidential guard personnel are occasionally found at sites, often in breach of the country’s mining code. The new unit will eventually replace the police, the IGM told Bloomberg in a separate message.

Congo is the world’s second-biggest source of copper and largest producer of key battery mineral cobalt. While those two metals are largely mined at massive industrial projects, most of Congo’s mines are dug by hand by millions of artisanal miners.

The U.S. hopes through the minerals partnership to convert peace and investment deals with Congo into influence over the country’s critical-minerals supply chain.

The U.S. has stepped up efforts to secure critical mineral supplies globally for a strategic metals stockpile as it seeks to reduce reliance on China and counter China’s dominance in Africa.

The U.S. is in the process of soliciting private sector feedback on the list of assets, the official told Reuters on Friday.

“We have significant interest, yes,” the official said, but declined to name the companies, saying “the conversations are still forming.”

LMEL eyes cobalt from Congo to India through US partnership

Nagpur: Lloyds Metals and Energy Limited (LMEL), which has taken over CHEMAF Group, a mining company in the Democratic Republic of Congo (DRC), early this month by forming a joint venture with US’ Virtus Mineral Group, plans to get its share of cobalt from the African nation to India as well.

The sharing formula would depend on the agreement between Indian and American governments as the venture also has a US partner. CHEMAF’s mines are seen as a major non-Chinese source of cobalt, a critical mineral, especially when India doesn’t have any major resources of the metal.

“The production is expected to start within the current fiscal,” said LMEL’s managing director B Prabhakaran.

The company projects an initial output of 20,000 tonnes of cobalt and 60,000 tonnes of copper a year from the Congo mines. CHEMAF Group has mines in Congo’s Katanga belt, known to be among the biggest copper reserves in the world apart from having sizeable cobalt deposits.

The takeover of CHEMAF Group by the LMEL–Virtus combine is also seen as a major victory for the US government, as it could outmanoeuvre the Chinese players who were also eyeing the company.

Fully focused on its goal of regulating the precious mineral sector, Félix Tshisekedi’s presidency expects significant fiscal returns this year. The authorities, however, have had to contend with pressure from Chinese operators eager to obtain larger quotas, as well as the reluctance of certain administrations.

Under the presidency of Félix Tshisekedi, the Democratic Republic of Congo (DRC) is aggressively reshaping its role in the global mineral market, specifically targeting the cobalt and gold sectors to maximize state revenue and economic sovereignty.

Fiscal Returns and Strategic Control

For 2026, the Congolese Treasury has set ambitious financial targets tied to its newfound status as a market “price maker”.

Projected Revenue: The government expects roughly $2.3 billion in public revenue this year from cobalt alone.

Market Influence: By implementing a strict quota system (capped at 96,600 tonnes for 2026), Kinshasa successfully pushed prices from $21,000 in early 2025 to over $56,000 as of April 2026.

Alternative Scenario: Authorities estimate that without these regulatory interventions, revenues would have been limited to approximately $617 million.

Friction with Chinese Operators

The administration is navigating complex relationships with Chinese mining companies, which currently dominate much of the DRC’s mineral extraction.

Quota Resistance: Major Chinese firms, notably CMOC Group, have vocally opposed the 2026 quotas, arguing they are too restrictive compared to their production capacity.

Processing Ultimatum: The Ministry of Mines is leveraging these quotas to force Chinese operators into local processing agreements, aiming to shift the country away from being a mere raw material exporter.

Audit of Legacy Deals: In March 2026, the government launched a comprehensive technical and financial audit of the Sicomines “infrastructure-for-minerals” deal to ensure compliance and fair returns.

Administrative and Geopolitical Hurdles

Domestic and international pressures continue to complicate the regulatory rollout:

Bureaucratic Reluctance: Delays in implementing new export procedures at the end of 2025 caused bottlenecks at key transit points like the Kasumbalesa border post, forcing the government to refine its administrative arrangements.

The “U.S. Pivot”: Under a strategic partnership signed in late 2025, the U.S. is pushing for access to critical minerals to counter Chinese dominance. This includes a 44-project shortlist handed to Washington in February 2026, creating additional geopolitical friction.

New Enforcement Measures: To counter administrative weakness, the state recently partnered with Quantum to establish a “tax brigade” for better oversight of mining operators.

Congo’s exports to China are already due to benefit from duty-free access to China from May 1 under an initiative covering 53 African countries.

The new agreement sets out cooperation on geological data sharing, investment protection and the promotion of local processing of raw materials in Congo, according to the Congolese government statement published late on Thursday.

It also includes a monitoring mechanism to ensure projects comply with Congolese law and are implemented in a stable and transparent investment environment.

Democratic Republic of Congo will enforce a long-dormant rule requiring local employee ownership for mines in a move that may rebalance shareholdings in some of the world’s biggest copper and cobalt producers.

In a letter dated Jan. 30 and addressed to miners of all metals in the country, Mines Minister Louis Watum said firms must demonstrate that 5% of their share capital is held by Congolese employees.

The decision could affect multiple industrial mining projects in the central African nation, which provides about 70% of cobalt supply and is the second-largest copper producer. Glencore Plc, CMOC Group Ltd., Ivanhoe Mines Ltd., Eurasian Resources Group and Zijin Mining Group Co. are among the country’s biggest miners. Barrick Mining Corp. operates one of Africa’s largest gold mines in the country, which also has vast deposits of lithium, tantalum, tin and zinc.

The move comes amid ongoing negotiations between the Trump administration and Congo that could see more US companies invest in the country’s mining industry, which has previously been dominated by Chinese enterprises.

JOHANNESBURG (miningweekly.com) – South Africa’s Exxaro expects to start mining iron ore in the Republic of Congo this year, with an eye to producing up to 10 million tonnes a year, as the miner diversifies beyond its traditional reliance on coal.